Hello Grasshoppa,

Recently, I delved into the latest appendix released by KWSP on EPF statistics. As a proud Malaysian and an EPF member, these stats spoke volumes to me. Here’s what I think after taking a deep dive into the numbers.

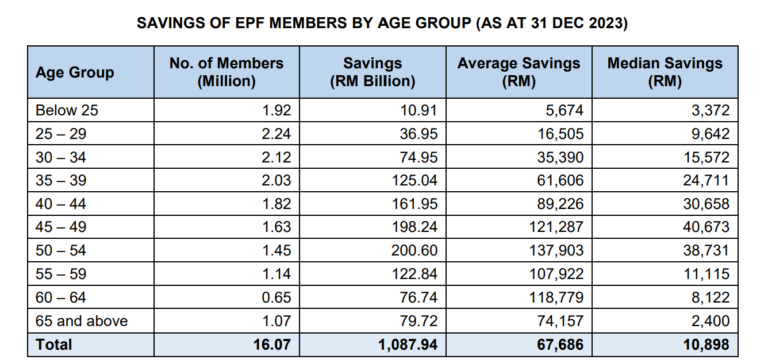

The main target age group I will be discussing is 25-29, a period when individuals are typically beginning their careers and contributing to their EPF savings based on their monthly income. As they move into the 30-39 age group, their savings should ideally increase as their income and career stability improve. However, it is surprising to see that the average EPF savings for members aged 35-39 is quite low. Another critical age group to consider is 50-54, as members have the option to withdraw their savings at 55. It is concerning to note that the average savings for this group is RM137,903. If we divide RM137,903 by 20 years (assuming a lifespan of 75 years), that amounts to RM6,895.15 per year, which is insufficient to cover annual expenses.

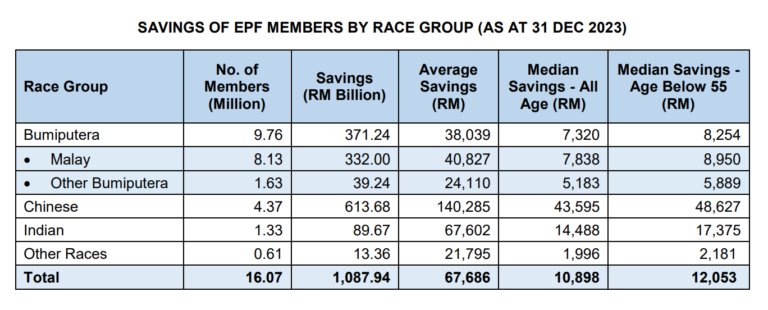

Based on the above statistics, it can be assumed that different races occupy various types of jobs, leading to different pay gaps. However, there is limited information to analyze beyond the assumption that each race holds different jobs with varying pay. I must acknowledge that my understanding of racial groups and pay gaps is not sufficient to provide a detailed analysis of these statistics.

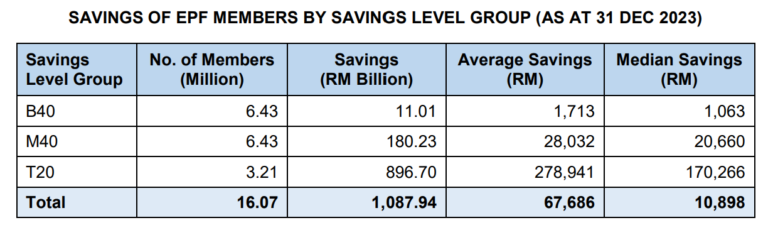

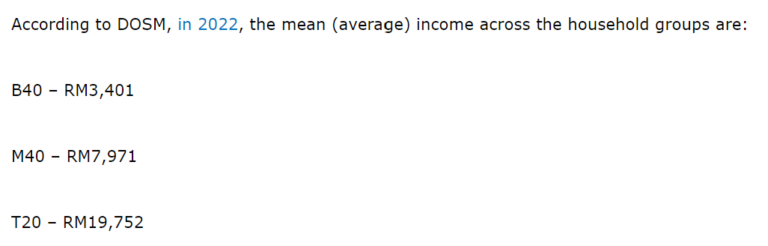

These average savings amount explains a lot of the pay gap between each level group. You may also check out this link by the Malaysians Employers Federation (MEF) on the average household income to understand the pay gap between each level group. Because the pay gap between each level group is high, you can see the difference between the EPF savings of each level group.

Conclusion:

Fully relying on EPF savings when you retire can be risky if you have average savings as per the above stats. If you have an alternative income or savings that you allocate aside from EPF, that will be helpful to you especially when you are retired but what is the ideal amount that you need to retire in Malaysia? Based on the previous recommendation by Tengku Zafrul, Malaysians need to have at least RM240,000 to retire. In my previous recommendation, the minimum amount that I recommend based on my calculation is RM900,000. This amount also is just enough provided if you have a good medical insurance plan while you are already planning ahead for your children’s education fund.

Can you actually achieve RM900,000 in savings by starting to work at 25 & retiring at 60? Assuming you work for 35 years, that means that you need to save RM25,714.29 annually. Look at your EPF contribution each year & ask yourself, what is the gap between your EPF contribution annually vs the amount that you need to save? If your EPF contribution has exceeded, good for you but if there is a gap, what are the other savings that you are saving to cover the gap? Options like Private Retirement Scheme (PRS) or other investment options can be helpful for you to fill up the gap. On top of that, your investment income is also a bonus for you to close the gap.

RM900,000 in savings at age 60 sounds not achievable until you break it down & you will notice that it is actually doable as long as you start saving & investing early. Start saving & investing early. You can do it.

OSS!