Hello Grasshoppa,

There are multiple debates that happened for the past few months by the current government & opposition about withdrawing EPF money for those who need fund to live through the challenging time like the current pandemic. Many of us are impacted by this pandemic in different ways & many have suffered from it. The current government has been taking multiple initiatives to help out as many Malaysians as possible like offering subsidies such as salary subsidy & many others. From April to September 2020, there is Moratorium financial relief by banks that all of us are benefiting from it. Many have tried to appeal for further extension but it seems that the majority of the appeal was rejected. A time like this is tough & utilising our own fund such as EPF will help during a situation like this.

1. Using Your Account 2 To Fund Your Housing Loan

I have written about the process of utilising your EPF account 2 in the past when I tried to apply it during early 2020 & I have also mentioned it during my recent interview with BFM. I personally think that lightening your burden at this moment is important as we do not know how long this situation lasts. Having extra money in your pocket will definitely help especially for those who are affected by this pandemic.

2. i-Lestari – Account 2

i-Lestari allows you to withdraw between RM50-RM500 monthly effective May 2020 to March 2021. You are able to withdraw up to a maximum of 12 months of your account 2 savings. All applications can be done online via the i-Lestari link.

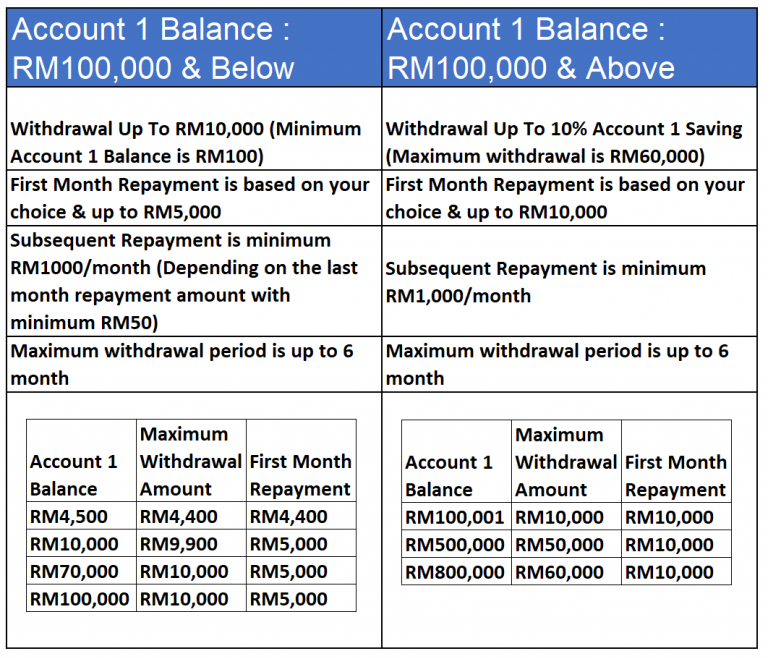

3. i-Sinar – Account 1

After multiple debates between the government & opposition, the government has decided to allow withdrawal of EPF account 1 for those who are affected by Covid-19 pandemic. The list includes those who have lost their job, lost 30% of their income or more, unpaid leave & no source of income. Currently, the application is split into 2 categories with Category 1 being able to apply effective 21st December 2020 & Category 2 effective 11th January 2021. You may refer below on the withdrawal eligibility :

Conclusion :

My personal recommendation is to utilise your account 2 for housing loan withdrawal where it can actually reduce your financial burden. If are affected badly by this pandemic, you may opt for both i-Lestari & i-Sinar package to help you service while the market recovers. Do not withdraw if you are looking to spend it on things that you don’t need as it will affect your retirement saving & yearly compounding dividend. All applications can only be done via KWSP official website & not other agent or web. The bad thing is, there are scammers out there that claimed they are KWSP agent & many Malaysians have fallen into that scam. Only apply via the official website or if you have any questions, you may visit KWSP office or reach them via their hotline.

OSS!