Hello Grasshoppa

We may have some Mutual Fund Agent friend that approach us to ask us to invest our EPF Savings to Mutual Fund. Their most common approach is to highlight that EPF Dividend is too little. Invest in Mutual Fund may generate higher return.

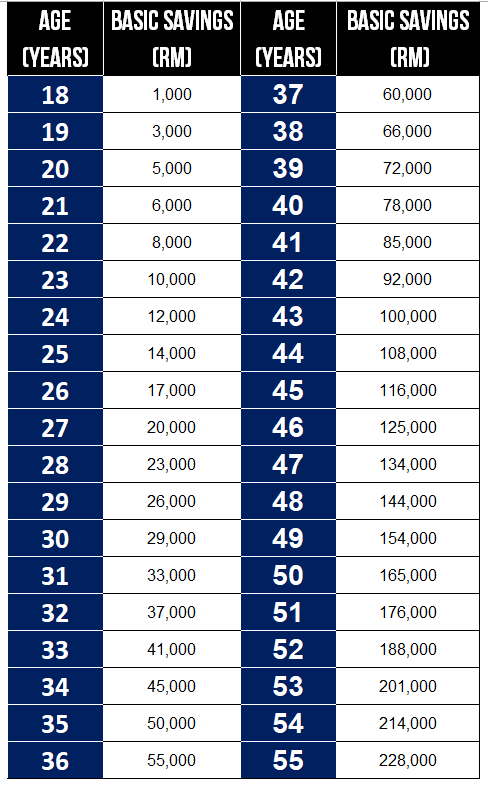

Before we compare EPF Dividend vs Mutual Fund Return, lets look at the minimum basic savings & EPF members eligibility. In order to withdraw our EPF savings from Account 1, we need to have MINIMUM Savings as below :

SOURCE : EPF

There are quite a number of Mutual Fund that allows EPF members to invest their money to the fund with minimum investment of RM1000. Withdrawal period will be every 3 month based on last withdrawal date. My personal experience for EPF withdrawals usually take up to 2 weeks & the process can be hectic. We are required to fill up EPF Withdrawal Form with our fingerprint & Fund Purchase Form. EPF can be really rigid when it comes to the fingerprint part.

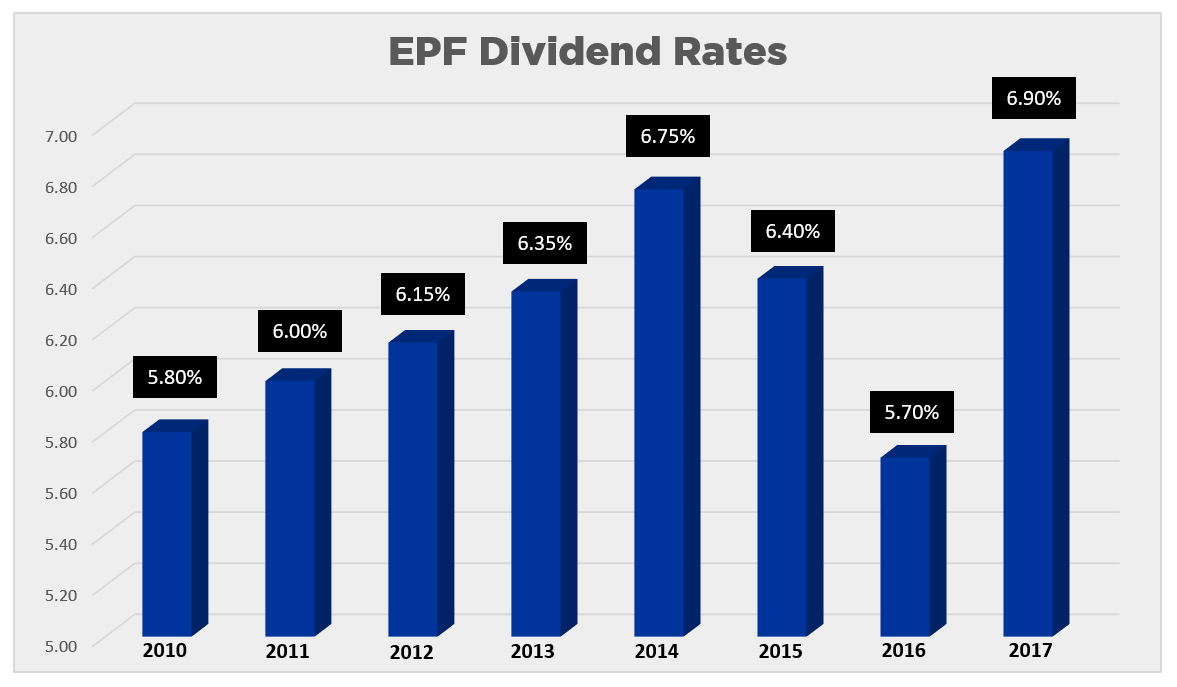

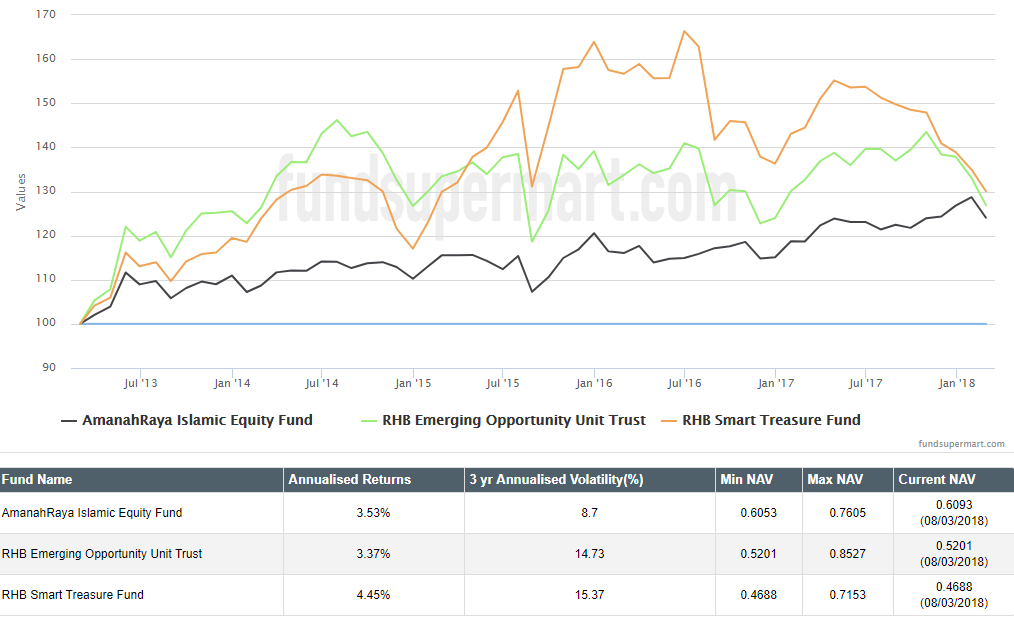

Now Lets Look At EPF Dividend Rates vs Top Recommended Mutual Fund By Fundsupermart :

SOURCE : EPF

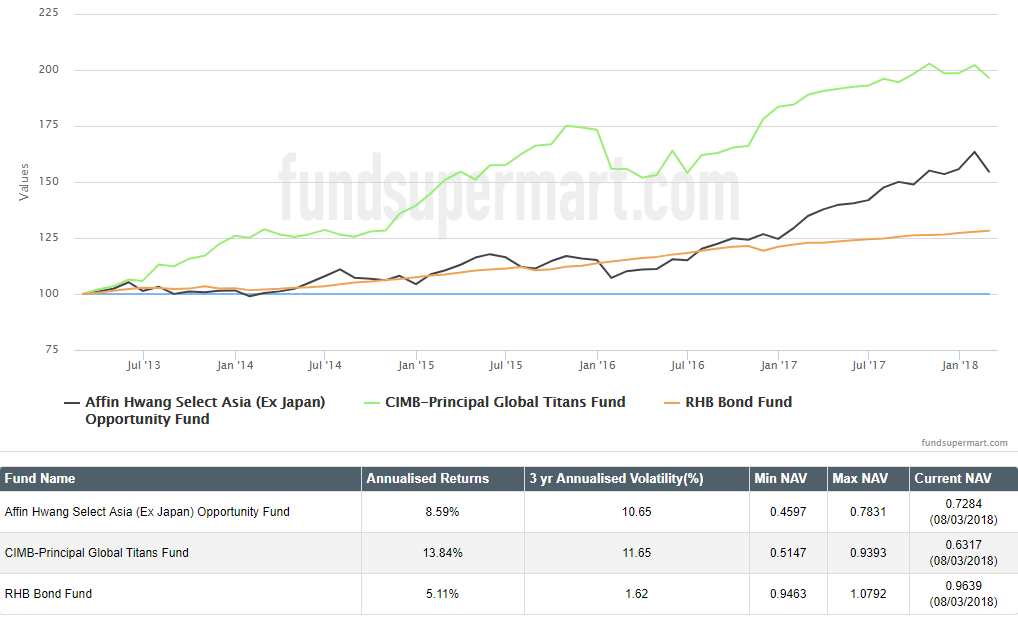

SOURCE : Fundsupermart

Looking at the Annualized Returns of the Mutual Funds, they are definitely a winner IF YOU SELECT THE RIGHT FUND. What if you select the wrong fund?

SOURCE : Fundsupermart

If you select the low performing fund, your Annualized Returns is lower than EPF dividend. Lets not forget Mutual Fund have Load Fee (average 2%) each time you purchase your fund. Each time you purchase the fund, you have to pay up to 2% from your investment amount.

Example : RM1000 X 2% = RM20. Means your total investment value is RM980 instead of RM1000. If you invest RM10,000, they will charge RM200 from your investment amount. Their Annual Management Fee is also something you need to watch out for.

Average return for EPF from 2010-2017 is 6.26%. In order to make 6.26% in Mutual Fund, first you have to add the amount that you pay for the Load Fee (2%). So its 2% + 6.26% = 8.26%. Average Management Fee for Mutual Fund is 1.5%.

Example : If you invest RM1000, first you have to pay the Load Fee (2%) = RM20. Lets say there is 0% Annual Return from your investment, you still have to pay Annual Management Fee (1.5%).

Fund Value After Annual Management Fee = Fund Value x Annual Management Fee

Your Fund Value for the amount you invest with 0% Annual Return is RM970.20 (RM980 X 1%=RM9.80). In order to match EPF Dividend Return, the Mutual Fund have to generate at least 9% Annual Return.

Conclusion :

Now when your Mutual Fund Agent tells you that EPF Dividend is too low & Mutual Fund can generate higher return, will you believe them? Of course there are Mutual Fund that are outstanding & outperform EPF Dividend but are you willing to risk your life savings?

AND NOW….

OSS!

Great post. Most people shouldn’t take out their EPF money for unit trusts. Many unit trust agents are just chasing commissions, and most investors don’t realize that apart from selling funds to them, the agents are not responsible for further advice or performance of those funds. I am a fairly competent investor, and even then, over the last 4 years with my EPF unit trust investments, I have only managed a 0.5% net average annualised advantage over EPF. One could argue that my performance was due to the timing. I started my EPF investment programme after the post-2009 local bull run had tapered off. But then again, even experts can’t time markets, so why should most EPF contributors?

Hi Kris. In my opinion, mutual fund is not a bad investment option but we have to factor in the potential risk & their management fee, load fee & other fee.