Today, we’re diving into a crucial aspect of financial planning in Malaysia: the Employees Provident Fund (EPF). Whether you’re a seasoned investor or just starting to explore your financial options, understanding EPF is essential for securing your future. In this comprehensive guide, we’ll walk you through everything you need to know about EPF and how to make the most out of it through strategic investments.

What is EPF in a Nutshell?

The Employees Provident Fund (EPF) is a retirement savings fund established by the Malaysian government. Its primary objective is to help employees save for retirement by requiring both employees and employers to contribute a portion of the employee’s salary every month. These contributions accumulate over time and provide a source of income during retirement.

EPF contributions are mandatory for most employees in Malaysia, with contributions made on a monthly basis. As of 2024, the contribution rate is typically 11% of an employee’s monthly salary for those below 60 years old, while for employees aged 60 and above, the rate is 5.5%. Employers contribute 13% for employees below 60 years old & contribute 6.5% for employees above 60 years old. EPF accounts are divided into two main categories: Account 1 (Account Persaraan) and Account 2 (Account Sejahtera). There is also an option where you can opt for Account 3 called Account Fleksible. Account Persaraan primarily serves as a retirement fund, with withdrawals restricted until retirement age or under specific circumstances. Account Sejahtera, on the other hand, allows for more flexibility and can be withdrawn for various purposes like education, healthcare, housing, or investment.

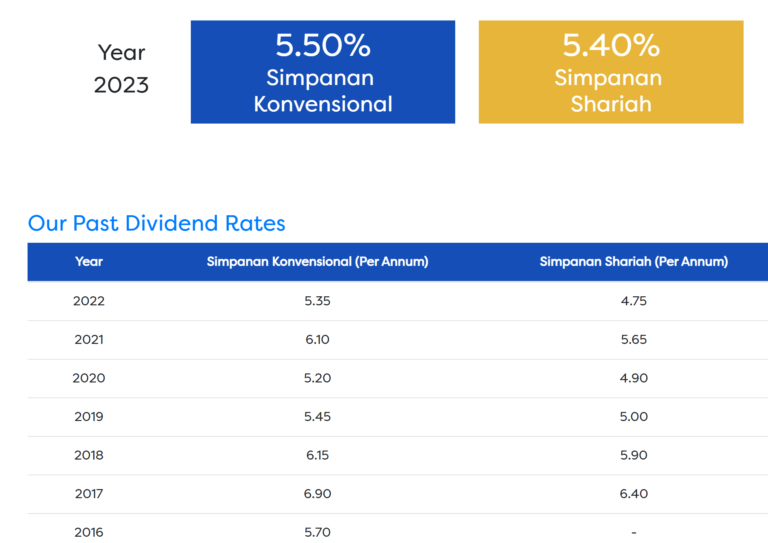

How Can You Use it to Your Advantage?Looking at the trend of EPF annual dividend return, EPF generally offers a stable annual return compared to other investment schemes such as Fixed Deposit (FD) or other medium or lower risk investments. During the pandemic period, FD rates have dropped to below 2% which makes it one of the lowest in recent years. With the EPF annual dividend rates, it is safe to say that we can expect the EPF annual dividend to be above 5%. That also makes us earn at least RM5,000 if we have RM100,000 in our EPF account.

For those who are looking to invest in EPF aside from their monthly mandatory contribution, EPF does offer self-contribution where you can contribute up to RM100,000 (previously RM60,000) to your EPF account. For gig employees or self-employed workers, you can contribute via i-Saraan. For husband that wants to contribute their EPF percentage to their wife, they can do it via EPF iSayang. EPF also allows you to use your EPF Account 1 (Account Persaraan) to invest in approved funds via i-Invest. If you are looking to manage a portion of your EPF funds at your own risk, EPF i-Invest allows you to do so in their list of approved funds. Bear in mind that there will be additional costs such as sales fees or other fees as those funds are managed by banks or other investment companies.

One of the ways that I used my EPF Account 2 (Account Sejahtera) was for my housing repayment. You can refer to this link to understand more about how can you use your EPF fund for your house. There are also ways you can utilize your EPF for your health protection such as insurance (i-Lindung) or other health-related such as fertility or critical illness. If you are looking to fund your studies, you can also use your EPF Account Sejahtera to fund expenses such as tuition fees, accommodation fees, or even one-way flight tickets for studies abroad. When you are 55 or 60 years old, you can proceed to withdraw your EPF savings in partial or full. If you are not in a rush to withdraw in full, you can utilize your EPF account to enjoy the annual dividend that gives you a stable dividend yearly.

Conclusion:

The Employees Provident Fund (EPF) is a cornerstone of retirement planning in Malaysia, providing a secure savings platform for millions of employees. Over the years of being an EPF member, all I can say is, that I am impressed by many of the initiatives introduced by EPF to help Malaysians in various ways such as i-Lindung, i-Invest, i-Sayang & other initiatives. By understanding the fundamentals of EPF and making informed investment decisions, you can maximize the growth of your retirement savings and secure a financially comfortable future. Take advantage of EPF’s fund wisely & make sure you utilize & plan your funds wisely for both the short term & long term.

OSS!