Hello Grasshoppa

When we talked about EPF, it will always be linked to our Retirement Savings. Do you know how EPF generate income to pay us dividend? Or do you know we can utilize our EPF savings for various purpose?

Employees Provident Fund or EPF was founded in 1991. It requires Employers & Employees to contribute towards their retirement savings. They are able to withdraw those savings during retirement or for special purposes only. Contribution rates for Employees is at 11% & Employers is at 12%. (13% if Employees salary below RM5000)

Similar to Fund Manager, EPF have their Fund Management Team where they will invest in various portfolio such as Loans, Bonds, Stocks, Private Businesses, Development & most recently USA 🙂

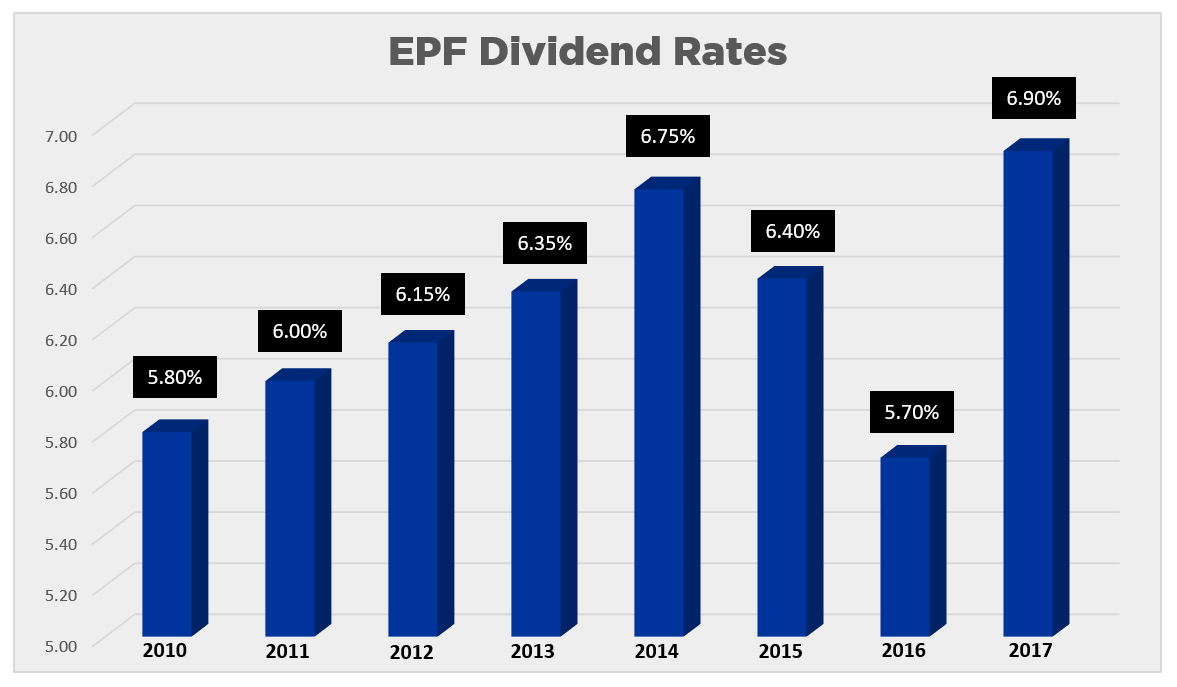

In 2016, EPF have introduced a new Retirement Savings option called Simpanan Shariah. Simpanan Shariah will be managed & invested according to Shariah Principles. All EPF members have an option to convert their Conventional Savings to Simpanan Shariah. They have declared 6.4% Dividend for 2017 vs Conventional Savings 6.9%. As for Conventional Savings, their latest Dividend is the highest since 1996.

Yes. Its a happy news to all of you right? 6.4%-6.9% dividend for 2017 Dividend Distribution.

How Can You Fully Utilize Your EPF Withdrawals?

- Education – You can use this to clear your PTPTN loan or your kids PTPTN loan. Aside from that, you can use this to further your studies or your kids Education Fees. This includes flight & hostel fees for the first year during registration.

- Haji – Age below 55 that have received approval from Lembaga Tabung Haji are eligible to apply. Maximum withdrawals via Account 2 is capped at RM3000.

- Disability – Any EPF member with permanent disability are able to apply this. Its subject for approval by KWSP.

- Leaving the Country / Migration – This applies if you have been stripped your citizenship or you have choose to forgo your citizenship. Any foreigner that works in Malaysia are eligible to withdraw once their working contract is over.

- Medical Fees or Equipment – Members are allowed to withdraw money from their Account 2 to pay for their medical fees or their family. Selected medical equipment are allowed under this withdrawal.

- House – Members are able to withdraw money from Account 2 to pay for their Mortgage Loan, Renovations, PR1MA Housing or Building their Own House.

- Investment – Do you know that you are allowed to withdraw certain portion of your money from Account 1 to invest in selected Mutual Fund? Yes you can.

Special Withdrawals or Retirement Withdrawals

- Pension – This is only applicable for Government Employees that have been granted pension status.

- 50 Years Old – Partial or Full Withdrawals are allowed.

- 55 & 60 Years Old – Full Withdrawals Any Amount & Anytime.

- Above RM1,000,000 – Members are allowed to Withdraw if their total savings exceed RM1,050,000 for their own management. Minimum withdrawal is RM50,000 & it can be done each quarter.

Back in those days, we only get to know our EPF savings balance by reviewing the statement that are only available via EPF statement machine which can be found at the nearest Credit Card Booth or EPF office. Now can access your statement by going to EPF website or via their mobile app.