Hello Grasshoppa,

Common question that I am getting from people that are in debt but still wanting to invest their money is, “Should I invest first or pay my debt first?”. If you are in debt, yet have the desire to invest, which will be your priority?

That was my question as well when I was paying off my piles of debts & was considering to invest. During that time, my understanding of personal finance was still vague where I was unable to determine which should be prioritized. Honestly it can be as simple as looking at the interest amount that you are paying for your debts vs the expected interest that you may get from your investments.

Pros of Paying Your Debts Over Investing

Look at your credit card statement. How much interest are they charging? Average credit card interest rate is around 15%. How often can your investment return be as high as 15%? When you own a credit card, your main priority is to pay 100% of your credit card spending & NEVER pay the minimum amount. Banks often make money from those interest rates from your credit card. Since card like BigPay is introduced, I do recommend you to checkout the perks of using BigPay.

Personal loan & car loan are often fixed so you can pay accordingly to the agreed timeline of repayment. As for mortgage loan, many people often opt for Flexi Loan so that they are able to pay more when they have extra cash. This will help to shorten your repayment period & cut down the interest rate.

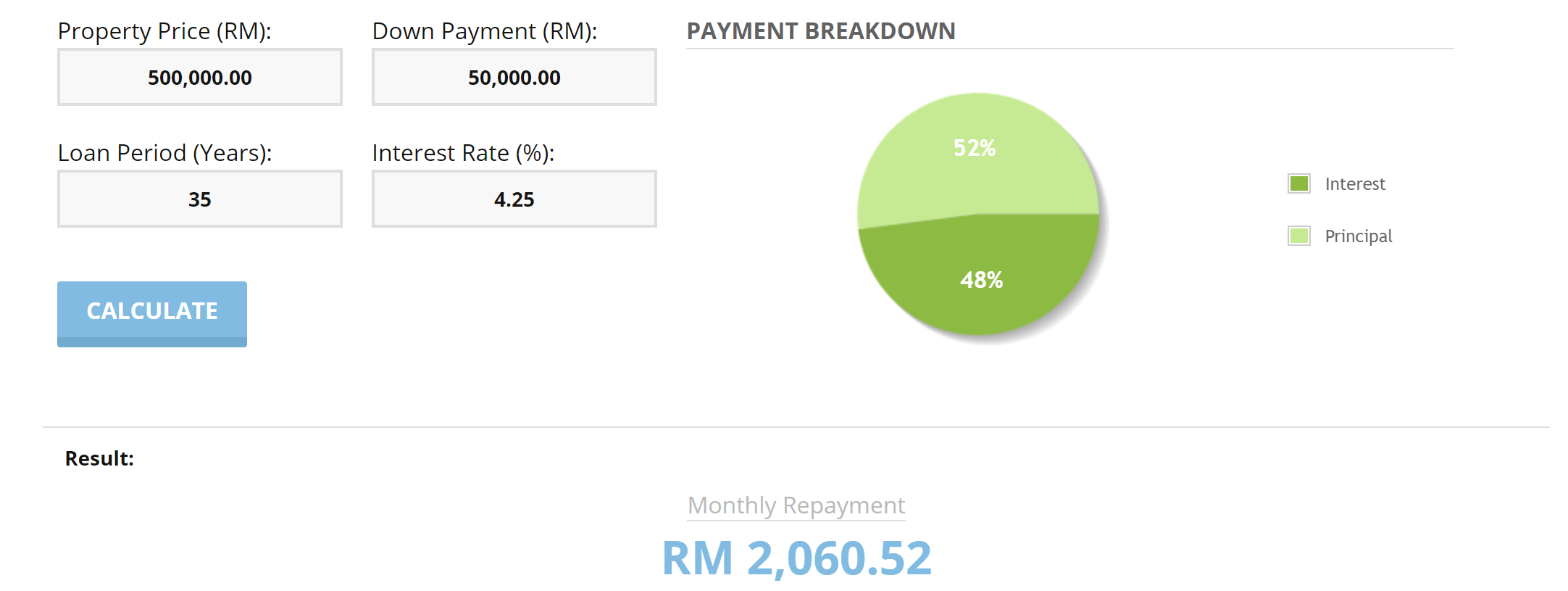

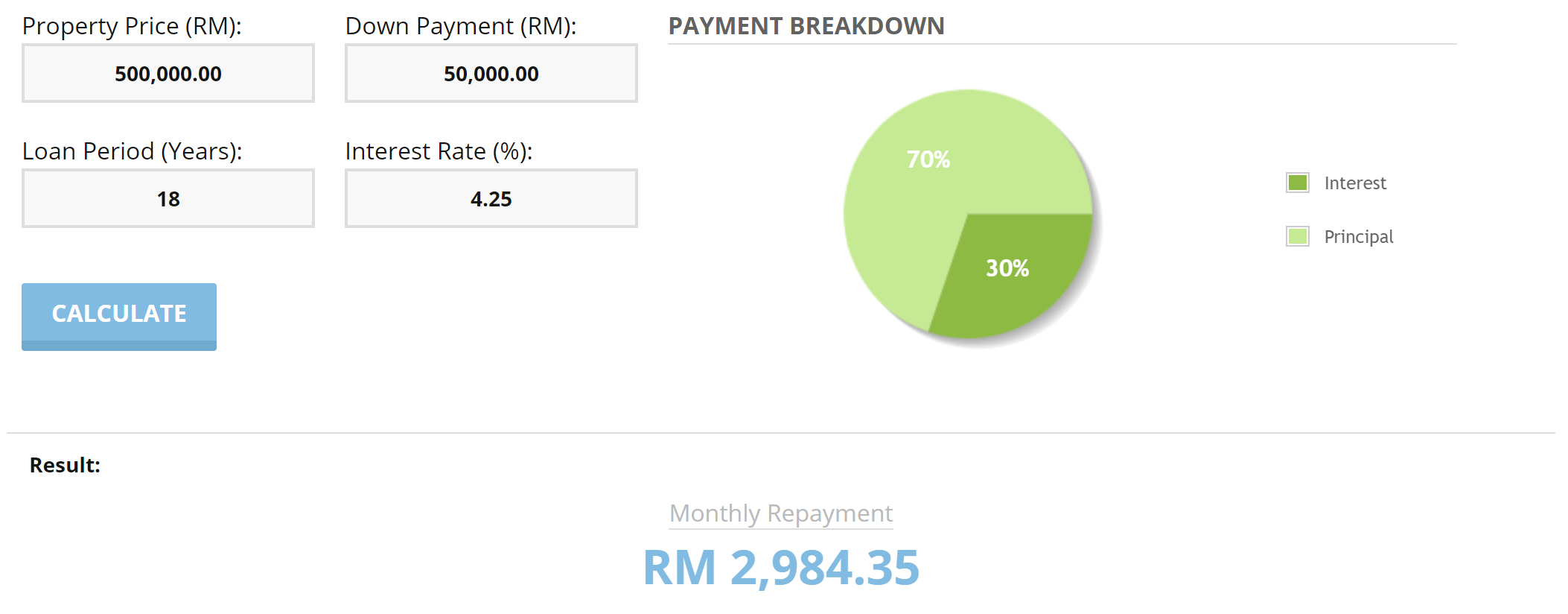

Let’s take an example of how much can you actually save from paying extra cash on your monthly mortgage loan. Below is a sample loan calculator for a RM500,000 mortgage loan :

35 Years : Your loan interest itself is 48% of what you are borrowing which means that you are paying extra RM415,419.65 on top of your RM450,000 loan.

18 Years : By paying extra RM923.83 monthly, your interest will be only RM194,618.56 which is 30% of your borrowing principal. That is a saving of RM220,801.09 by paying extra for your monthly loan.

18 Years : By paying extra RM923.83 monthly, your interest will be only RM194,618.56 which is 30% of your borrowing principal. That is a saving of RM220,801.09 by paying extra for your monthly loan.

Pros of Prioritizing Investing Over Your Debts

Investing can be volatile but long term trend is usually uptrend based on previous history. You can refer below S&P500 trend from 1990 – 2019. The trend is volatile yet it is moving towards uptrend. The question is, can you withstand a volatile market? Or are you investing in the right investment? There is definitely no guarantee in any investments whether it is stocks, mutual funds or any other investments. Imagine if you started to invest in year 2000 where it was trading at $2246 & you hold it until 2019 which S&P500 is currently trading at $3006. How much volatility that it went through from dropping below $1200 twice before it went to new high.

Conclusion :

If you ask me, I personally would recommend clearing off your debts first prior to investing. It would be better if you can have a balanced between both debt & investment. It all depends on what type of debt that you currently have. If it is credit card or mortgage loan, it should be prioritized over the fixed debt such as personal loan or car loan. If your mortgage & other loans are on the right track, you may consider growing your money by investing.

OSS!

I have been trying to clear off my cc debt for a while now. Always pay above minimum as best as I can (min 1k, Pay 1.5k) . But never really could make much of a dent. Only at the end of last year when I started using BigPay to pay for my auto debits ( 2 phones / 2 insurance ) then I started to see a steeper decline in my cc debt. Now my min is less than RM800.

Thank goodness.

So for me, clearing off debt is priority over investment. Thinking back, so much wasted interest!

Hi Gerald. Totally agree on this. Debt should always be the priority unless we have extra cash & debt is decreasing. Stay safe buddy.